|

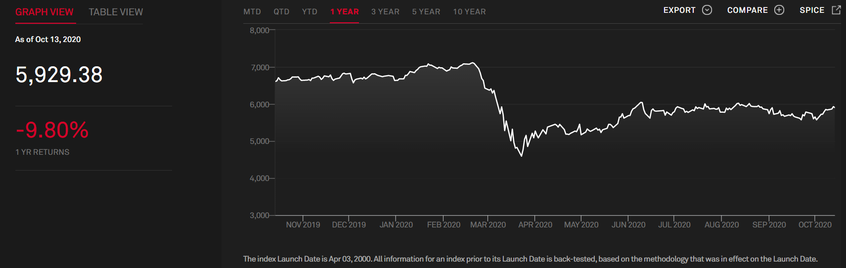

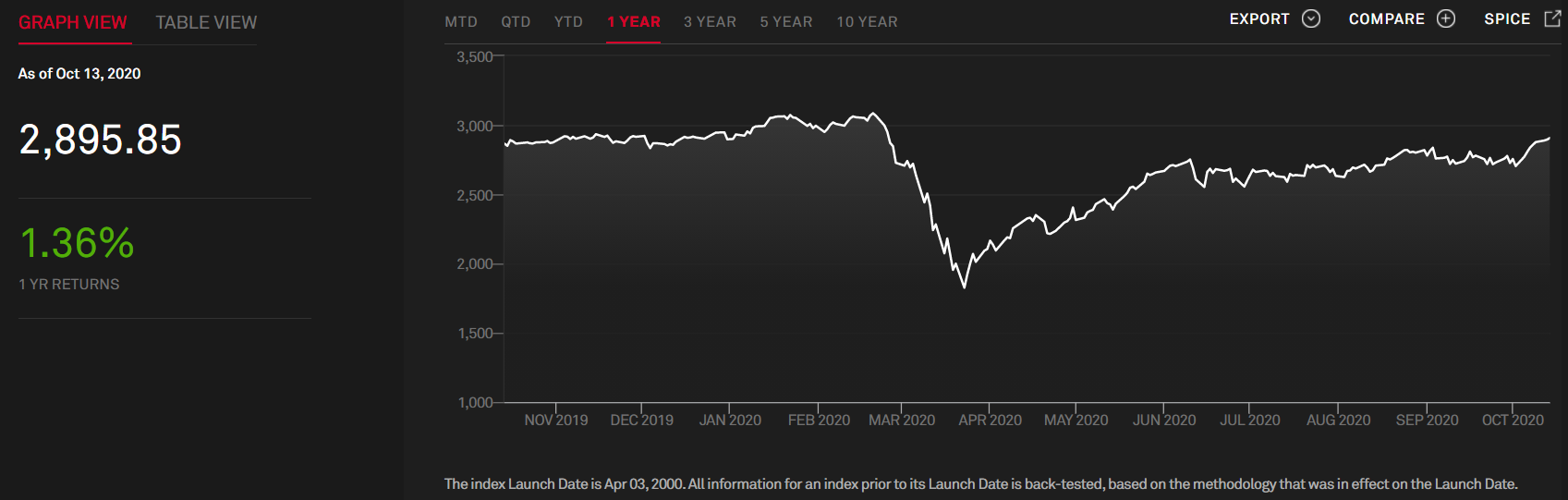

Following on from the exploration of the ASX20, I would like to visit the topic of large caps vs. small caps. What has been apparent in a world of low interest rates and QE has been the stellar outperformance of larger companies over smaller. On an intuitive basis this makes sense, since a negative economic environment should benefit larger companies who should, unlike their smaller counterparts, have the balance sheets and immediate access to a lower cost of capital to ride it out. Large caps often benefit from a flight to perceived safety during uncertain times too, though this may not be the case at the moment. So why hasn't this been the case in Australia? For Context: Broadly speaking, a “small cap” is considered anything with a market cap between $300m and $2bn USD in the global context. Of the almost 2,200 companies listed on the ASX, roughly 150 companies exceeded or hovered around the $2bn AUD mark to begin this financial year. This is to say that, even being very generous in leaving out currency conversion (you'd lose another 40-odd companies), only about 6-7% of the ASX was considered even a mid cap stock in the global context. A small cap in the context of the ASX is typically considered as those between $50m and $500m AUD (a mark which only 250-300 ASX-listed companies exceed). On a global scale, a large-cap is usually considered as those companies with a market cap north of $10bn USD. Give or take a few stocks, the ASX50 is essentially composed of companies with a market cap north of $10bn AUD. Forgive me for the overly general nature of this context section. These definitions are arbitrary and the constituent stocks are obviously affected by share price and currency movements on a daily basis.  Author: Sid Ruttala Author: Sid Ruttala The heavy lifting of the large caps is perhaps most evident on the NASDAQ where much of the recent push up has been led by the FAANG’s and the ever controversial Tesla. But that is on a global basis. For Australian investors this might not be as evident and is, in my opinion, unlikely to change. I come to this conclusion after spending a few weeks researching and understanding the balance sheets of the top end of the ASX. The behemoths of Australia basically all hail from three sectors 1) Financial Services; 2) Materials and 3) Telecommunications, all sectors that do not see significant advantages in the current environment. In fact, financial services is one of the worst performing sectors globally. If you break down the top performers on the S&P 500 globally they are solely high growth technology and healthcare stocks (at least 55% of the overall return). Even within the smaller companies, as shown in the graph below, the outperformance of the Russell 2000 index was in Growth while Value has remained overwhelmingly negative year-to-date and on a 3-year annualised basis. Sectors perhaps explain the rather underwhelming performance of ASX, what we in the office like to say follow the downside and underperform on the upside (i.e. we will certainly follow US futures down with a vengeance but say no thank you for the returns on the upside). In a liquidity driven market where things become excessively correlated, even the higher growth performers that are seen as beneficiaries and thus rewarded with higher multiples than would otherwise be the case, are disproportionately impacted in a sell-off since the negative performance of higher market weightings can draw the overall index down (Index funds perhaps further exacerbating this tendency in a small market like Australia). So, what does this mean for Australian investors? Would they be better off focusing on small caps? For one, look at the graphs below, the first showing the ASX50 and the second showing the ASX Small Ords. ASX50  Source: Standard & Poor's ASX Small Ords  Source: Standard & Poor's Based on the graphs above, the simple answer might be yes, but there is a caveat in that history has not been on the investors’ side. In the long-term picture, if one were to define it as the period from 1990 to the very recent past 2016, the small cap index underperformed by around 2.8% (since 1990) and has done so with 25% more risk.  Source: Schroders, Global Financial Data. Returns from 1 Jan 1990 for S&P/ASX Small Ords and S&P/ASX 200 (All Ords before 1/4/2000). There are a plethora of reasons for this (which remains quite an outlier when compared globally). Australia has historically been a less dynamic market and, to be honest, a safe-haven of sorts for the old-fashioned dividend-hunting investor. Think, for example, about the top thirty S&P500 stocks in 1990 and think about the top thirty now, do the same for Australia and you will understand my logic. Consider (for the older generation perhaps) the giants of the 20th century, Kodak, Xerox or Ford (the list goes on) and now consider their positions today. For Australia, the giants of yesteryear mostly remain the giants of today. The point I’m getting at is that larger companies here may have been safer bets than would otherwise be the case in a traditional capitalist system. There are about 150 species of fauna considered endangered or critically endangered in this country, perhaps none are more protected than the big banks.

On the flip side, the small cap space is hampered by the lack of a mature venture capital industry (and associated listing rules) and the fact that the materials and junior exploration (the vast majority of which are not cash flow positive) sectors make up a substantial portion of smaller companies. This means that the risk-reward metrics from a traditional portfolio construction perspective are off kilter. However, for the more discerning investors this does create substantial opportunities away from index-hugging. Not to mention substantial room for active management to significantly outperform given the associated inefficiencies (this is the only place where active can truly outperform, by the way). Bottom Line: We will continue to see the comparative outperformance of smaller companies given the sector composition of the ASX. However, the smaller companies space within the ASX is prone to inefficiencies and adds substantial room to remain active. This will be somewhat the opposite of global markets in that the low-interest, low-growth environment should see larger companies benefit disproportionately depending on the index (Canada, for example, is quite similar in composition to Australia). This potentially makes it more rational to 1) allocate by sector; 2) make more room for passive on the Global front; and 3) to be more active on domestic equities, shifting away from the top end, given the nature of the ASX.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim