|

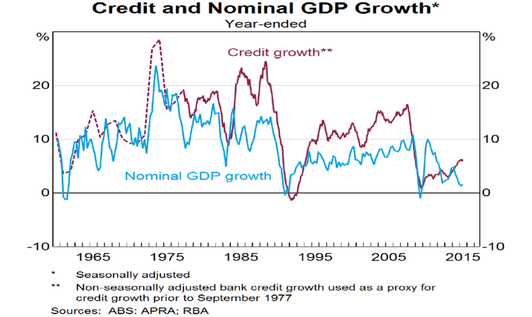

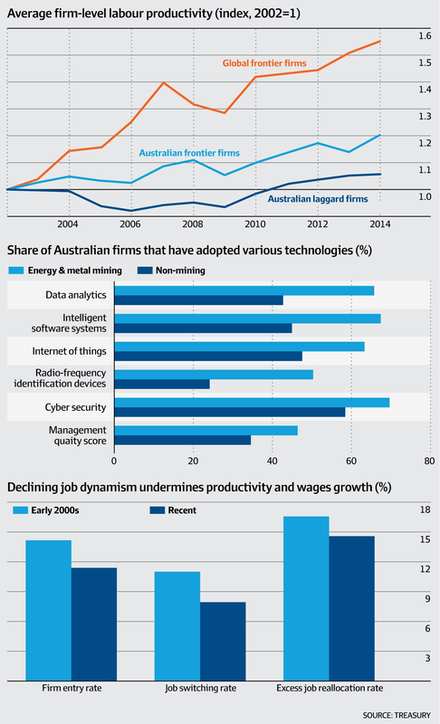

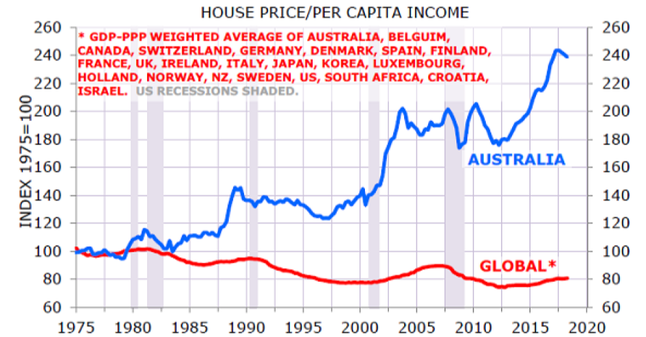

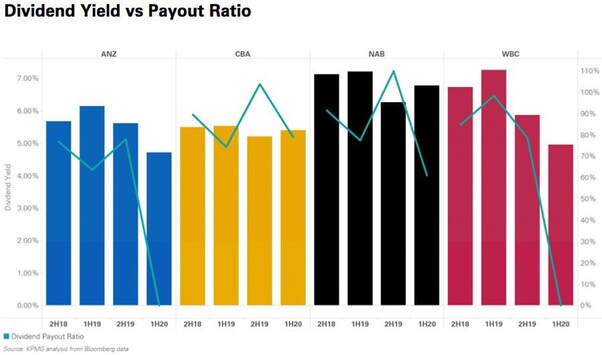

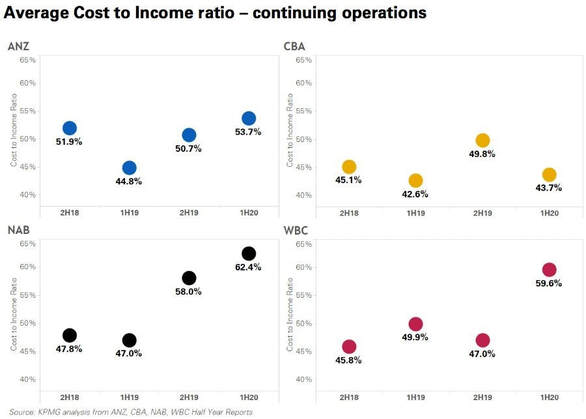

This week we revisit the most over-researched and perhaps over-discussed sector in this nation, namely the financial sector. More specifically I would like to touch upon the short-to-medium term outcomes of recent policy decisions.  Author: Sid Ruttala Author: Sid Ruttala I am sure most of our readership has some exposure to at least one of the Big Four. And most are aware of the direct hit to profits (to the tune of 40%, if one is to trust the numbers put out by KPMG), the cutting of dividends and the overall short-term mess as a result of Covid. So, rather than tell you what you already know, I would like to approach it from the context of an outsider looking at their role in the economy, the incentives of policy makers and the likely evolution that could occur as a result. Context The number of times I hear people, often people that should know better given their profession, confuse credit with debt is rather frustrating. So, let us begin with distinguishing between the two. Simply put, credit is the money available to be borrowed whereas debt is the actual money borrowed. When you use credit, you create debt. This might seem a rather diminutive distinction to make but it is one that is exceptionally important.  Source: ABS, APRA, RBA Note: The above chart is a few years old now, but one can easily see the historic correlation between credit growth and that of GDP. In a world of low-wage growth, the short-term output (whether one looks to the property market or elsewhere) is contingent on the ability to borrow. With the cost of servicing said accrued debt the primary driver of output rather than productivity. In fact, across the OECD and Australia the average per annum growth in productivity has been subpar at 0.9%, the average in this nation slightly better at 1%.  Source: Treasury But what does this have to do with the banks? For one thing, they are the primary originators of new debt and, as such, are fundamental to ensuring that growth (at least on a nominal basis) can occur. This is precisely the reason why the government and policy makers are intent on ensuring liquidity in the system. The ultimate too big to fail scenario, in which the Australian Office of Financial Management (AOFM) acts as a backstop by buying up mortgage backed securities, the RBA reduces the cost of lending to SMEs (Small to Medium Sized Enterprises) through reductions in wholesale funding costs to the tune of 25bps (0.25%), and the actual cost of holding Exchange Balances (ES) - the rate of return for holding excess reserves at the RBA - to 10bps. Meaning that the opportunity cost of taking on credit risk is 0.10%. It is the same reason the government, when it unveiled its financial ‘bridge’ to help the economy, decided to provide low-interest small business loans through the banks that would be 50% guaranteed by the taxpayer. Let us for a moment forget the ethical conundrum of letting private institutions have their risk be mitigated by the taxpayer and ask ourselves the question of why this was actually required? The answer I would posit is not simply about a short-term fix for a left-field event but a realisation that credit and the cost of debt are the only factors that impact overall economic growth in the short-run. The most obvious example of this, as the graph below shows, is the average house price in this country vs. per capita income. So, wages aren’t growing but the average cost of a dwelling goes up disproportionately, wonder why? It is a conundrum as to where the demand is coming from.  Source: Dallas Federal Reserve, NBER; Minack Advisors  The Results So Far So far it must be said that the monetary and fiscal measures implemented have been effective in ensuring that the availability of credit has not dried up as well as ensuring that banks are able to work with the government in order to reduce stress on borrowers. This, by the way, is not from some misguided sense of social responsibility though, as shareholders who have seen their dividends cut, it might seem like it to some. It is for the simple reason that having distressed assets is neither profitable or rational in the long-run. Having borrowers sell their houses or having foreclosures as a result of not being able to keep up with mortgage payments will have a broader impact upon the property market and the profitability of the balance sheet. From the government and monetary perspective, this is the reason why neither can actually afford the property market to rationalise let alone have it fall. It makes up too big of a component of the nominal wealth of Australian households, employs too much of the economy (15% of this country is employed within the construction sector), and roughly a quarter to a third of the ASX (read Big Four) derives a large chunk of its revenue from mortgages. If that were not enough, most SME lending is based upon personal guarantees and private property assets put up as collateral by the owner (we should know since we operate in this space as well). Even small revaluations of the property market through mark-to-market would have disproportionately adverse consequences within the financial system. Where To? Thankfully for the investors, the RBA has ruled out the European scenario of negative interest rates. This is not enough, however. Even beyond recent events, the nature of the banking/lending system has changed. More so than ever over the last few decades (think tightening of lending standards for banks, non-bank lenders, and most recently the emergence of BNPL). The Australian banks are unique in comparison to their global counterparts (with perhaps the exception of Canada) in that although they are well-capitalised (perhaps some of the best in the world) they are heavily concentrated in terms of their balance sheets. Their revenues primarily come from the residential mortgage book and their institutional business lagging in comparison to the likes of JP Morgan or their Asian counterparts like HSBC for example. From a risk perspective, one can expect that they are effectively guaranteed by the government (in the words of Tamim's Managing Director, Darren Katz, “There are two protected species in this country and they aren’t the emu and platypus; rather the banks and the property market”) but a low interest rate environment with increases in the cost of capital means margins should decrease (though this might be temporary as they invest in technology and the fallout from the seemingly now forgotten Royal Commission). Contracting Net Interest Margins (NIMs) can have a traumatic impact in the long run as is evident in Europe and their Japanese counterparts. Unfortunately for Australia, they don’t have the advantage of US banks who can underwrite with the reserve currency. Simply put, yes they are (at this stage) a form of risk-free return. That is, if one limits themselves to market risk, ie the possibility of an investment going to zero. Are they going to be as profitable as they were historically? Probably not.  Source: KPMG  Source: KPMG How Is This Likely to Evolve?

I’ve heard recently the idea that, given the centrality of the property market to the Australian economy, that it might be plausible to implement our very own version of Fannie Mae and Freddie Mac. After all, the AOFM is already buying up Mortgage Backed Securities and the effective subsidies like the first home-owners grant aren’t that much of a stretch from the US version. But somehow, if one can effectively guarantee 50% of SME lending (typically property backed anyway), subsidise first home-loans, get rid of property taxes, securitise mortgages and facilitate a secondary market, aren’t we basically already there? Where does it stop? Our call is that the can will be kicked down the road indefinitely (at least if the indefinite can be defined as our collective lifetimes, the unborn can’t vote or speak…yet). Thank you, vagaries of three-year election cycles. For us investors, the music is still playing and let DJ Lowe come to the rescue if the dance floor is a little empty.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim