|

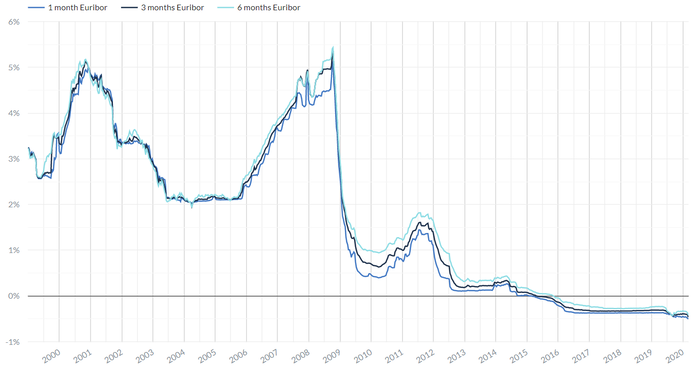

This past fortnight we have seen a lot of panic buying (mostly toilet paper and pasta) and selling. But why? Are people being rational or just following the herd? This fortnight has been rather eventful, but then again when have the markets not. We went off with a bang with the Fed cutting rates by 50 bps and the RBA with its own 25 bps cut, taking the cash rate to a stellar 0.5%. We must admit that when we made our 2020 predictions back in January we did not expect some of them to come to fruition quite so quickly. Though the prediction was for a further two rate cuts through the year we did have a running bet in the office that the cash rate would fall to zero by the end of the year. Those who took up the opposition position now officially wished to reconsider said position, we now expect a total of three cuts with the next one coming as soon as April. This brings forth the next question, what does this mean for the markets? We have seen UBS come out with the suggestion that Australia will have its very own QE (to the tune of around 50bn AUD) and, on the fiscal side of things, the government of the day suggesting that their fixation on getting back to surplus might very well disappear. Again, something we suggested late last year. We would go so far as to say that this is the start of a global trend and, in the absence of inflation, we are unlikely to see governments faced with electoral cycles change tack. What has been rather confusing has been the sheer amount of volatility that the past fortnight has seen across all asset classes. One of the more interesting trends has been the combined sell-off in both equities and safe-haven assets like gold. In the instance of gold it might have been rather precipitous since the only reasonable explanation we can offer in this instance is that it was a sell-off to cover the losses in other asset classes, most notably equities. So with that setup we seek to answer one simple question this week, where to next? Is it another meltup or the long dreaded yet much awaited meltdown? (Incidentally, there are a number of people we speak to who have been insisting we are mere months away from this meltdown for a few years now). Let us start by saying that we do not have a crystal ball. Valuations are stretched from a historical standpoint and yes there is a lot of uncertainty (not necessarily risk) in the markets. But try doing a DCF (Discounted Cash Flow) analysis with a risk-free rate of return of 0.5% and things get a little more interesting. In fact, if we were to go towards zero or even negative interest rates, then nothing makes sense. Hypothetically the valuations go towards infinity and therein lies the conundrum. What will be even more interesting is if the central bank locally follows its European counterparts. In which case, we are likely to see a transformation of the investment process all together. We’ve previously written about the curious case of Austria issuing its first 100 year bond whose capital value appreciated close to 80% within the space of a year. What this suggests is that we are entering unprecedented territory where bonds are essentially seen as creating tax events and one looks to equities for income. Think through that for a minute where the capital appreciation of a sovereign bond has the same capital growth as that of one of the WAAX stocks. Or if one is not imaginative enough, have a look at the graph below for the Euribor which entered into negative territory. The Euribor, much the same as the LIBOR, is the interest rate for the wholesale markets (i.e. the rate at which banks lend to each other).  Source: MacroVoices Presentation, Francesco Filia  Source: euribor-rates.eu Or in fact consider the graph below which showcases the yield on Nokia debt, rated BB+.  Source: MacroVoices Presentation, Francesco Filia When bonds enter into negative yielding territory one cannot really call them bonds. They are anti-bonds or whatever other term you would like to attach to them. The name of the game is now hot potato. If equity markets get a little volatile, money floods towards the bond market, not in the expectation of deriving income but rather with the expectation that central banks, with their vaunted balance sheets, are able to bail them out of any disaster situation (the ultimate put). The moment this ceases to be the case, there are then a plethora of flow on effects including both price and duration risk. So why should you care? So why the whole spiel about bonds and what is the caveat? For one thing, we want to illustrate just how strange of a phenomena we are seeing in the markets. The countless number of times we’ve heard that we are in for another GFC like scenario never gets old. The naysayers may very well be right to an extent but there is a fundamental difference when QE and other unconventional tools are brought into the picture. For one thing, through the DotCom crash and the GFC bonds acted as a buffer with an inverse correlation to equities. Think about the markets as moving parts. If you take out that buffer and add in the potential for negative rates in cash, then as an asset class equities is potentially the only place to be. No, not a choice but the only place. Which is potentially the logic of policy makers, whereby these mechanisms, at least theoretically, should force capital to be allocated towards risk. Rising equities valuations and the decreasing cost of capital are, in theory, supposed to incentivise capital expenditure, inflate wage growth and boost consumer sentiment. They seemed to have forgotten a little thing called incentives though; businesses are run by people, markets are made up of people. They apparently didn’t realise that a lower cost of capital could just as easily be used to buy-back shares, push up EPS on paper and lead to increasingly sky-high valuations with no real impact on the underlying economy. Add in some fundamental differences, like the increased use of passive strategies and lack of actual price discovery, and these problems are exacerbated. Investing in this world is one massive momentum trade where companies are incentivised by share price growth and quantitative strategies rule the day. For example, a 5% dip should, in the absence of human interference, automatically result in bids from algorithmic trading strategies (algos). This and the increased use and proliferation of technologies, from passive ETFs to the democratisation of markets for retail investors, has created a scenario where the cost of trading is driven downwards but hot money has increased. These factors are perhaps the reason that we see mini-crashes like the December 2018 where equity markets lost close to 20% in a single month. The quest for daily liquidity has also resulted in a scenario of creating self-fulfilling prophecies where, in the event of even slight downturns, the problems are further exacerbated both on the downside and the upside. What is truly scary is what one investment manager by the name of Fransesco Filia, of Fansanara Capital, called the ultimate margin call. In the event of a panic sale with daily liquidity, it could potentially lead to $2tn to $4tn sale in a short period of time. How did he get these numbers? He simply took the assets under management (AUM) of the top three fund managers globally (BlackRock, Vanguard and State Street) with 17.2tn USD under management and a 20% selloff... resulting in panic selling effectively draining 2-4tn in liquidity. This is the reason why the Fed intervened in Q4 2018 and the reason why we find it very hard to bounce out of this situation. Now think through that for a minute and the amount of strain that puts on the global financial system, Lehman would pale in comparison.  So where to next? By all means, take this with a grain of salt given that we are an equity manager but we truly continue to believe that equities are the only asset class to be in. Buying the right companies at the right prices should protect us over the long run both in terms of inflation and uncertainty. On a rational basis, understand that owning equities is owning businesses not numbers or a ticker code. Businesses with real people thinking through the same problems as the rest of us. We don’t know about you but we would rather trust in well-run companies with good management to guide us through any economic uncertainty rather than hold out hope that the rest of the world is not seeing what we are seeing. That’s not to say that you should be aggressive, but be rational and reasonable. Diversify sensibly across asset classes and sometimes even real assets. For example, in the event of economic headwinds and low interest rate environment, how does infrastructure perform? We would say very well, especially as governments spend more. If inflation were to pick up steam again as a result of fiscal expansion and interest rates cannot be raised because of the reasons previously mentioned, how would gold perform? We would say very well. If the COVID-19 gets out of hand and becomes a major pandemic, how would technology stocks such as Zoom Communications (work from home conferencing) perform? Very well, we would imagine. The point? Don’t panic, understand what you own and how they intend to solve the problems. We would suggest that it is foolish to divest yourself of your equities, good companies will recover and continue to generate profits over the long term. We are seeing the panic buying of toilet paper in Australia right now, the most telling part of it all? This lady quoted by news.com.au: “I’m buying it because everyone else is doing it”. Australia produces enough toilet paper domestically that there likely wouldn’t be supply issues without unnecessary panic buying and hoarding. When it comes to panic buying (or panic selling when it comes to equities), people tend to become sheeple and follow the flock without fully understanding why. So, when it comes to both toilet paper and equities we are saying be rational, do your research and make appropriate and logical decisions. Cash is not king, it is a liability and a promise from a sovereign government. If you don’t wish to believe us, Zimbabwe might be an exceptional example or, for the history buffs, the Weimar Republic. All this being said, keep in mind this quote by Keynes: “Markets can stay irrational longer than investors can stay solvent”

3 Comments

Richard Manuell

5/3/2020 05:20:28 pm

Excellent article: we should not panic, but continue to act sensibly.

Sid Ruttala

9/3/2020 10:16:34 am

Hi Richard. Thanks for the feedback. We've seen the underlying impact of these policies through the broadly increased income and wealth inequality across the Western Economies. In terms of the accounting side of things, in this instance there is no debit for the credit side of the equation. Not when fiat currencies are involved and not when institutions (in this instance Central Banks) can theoretically go into negative equity and still not go bankrupt.

Wesley Horn

3/4/2020 04:17:51 pm

Hey Richard, be assured every debt does not have a matching credit in this world. A friend of mine once offered, it's a zero sum game isn't it? No, it's definitely not. Many years ago, I also used to ask, if particular countries are in debt, who's got the money? The world is very much in net debt. It's as simple as that and an explanation without bamboozling you with jargon. Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim