|

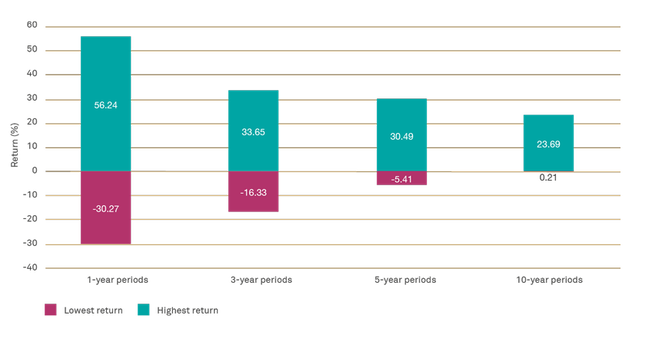

Following our 10 Principles to Invest By for the long-term, we thought we might once again try and grapple with some concepts and principles that we would have liked to impart to our younger selves.  Author: Sid Ruttala Author: Sid Ruttala For the fine wines amongst our readership, only getting better with age, these may be the same pearls of wisdom you wish to impart upon to the next generation, they may not. However, a disclaimer for those of you looking for a rather more substantive piece to read on current events, move on, because this is back to basics which some of you might roll your eyes at. The basics are the foundation upon which everything is built though. Like a sportsperson, the fundamentals must be developed and maintained as the base one develops the skills to truly excel. An elite scorer in the NBA might be amongst the best scorers of all time (useful when the objective is to try and score more points than the opposition) but if he isn’t a fundamentally sound defensive player, then you have an issue. Take current player Lou Williams, in his 16th season, the NBA's career leader in points off the bench. He lacks the fundamental skill of defence. As such, he has only started 118 of 996 career games (73 in two seasons alone) and it is a genuine question if you want him on the court late in a tight game… think about that, one of the elite scorers of the last decade potentially being left on the bench at a time when each and every point is at a premium. The point here is that if someone like that had all the fundamentals at a baseline level then you are looking at a different career trajectory entirely. A shaky base does not mean you won’t have success or lower your ceiling but it does typically put a floor in place while also potentially raising the ceiling. If you want another sport, think Nick Kyrigos and his temperament. No one denies his talent but his temperament (absolutely fundamental across most disciplines and something that can be improved and developed), while not stopping him from reaching the heights of his field, has meant he falls short more often than not. You could fluke your way to outstanding returns for a few years as an investor but, without keeping the basics in mind, it is likely you will be tripped up by things like simple cognitive biases at some point. This is an article focused on building and maintaining the foundation, raising the floor. So here we go. 1) The world is not linear Too often as humans, we fail to perceive the dynamism and uncertainty that is the real world. The economist in me comes up with models to make sense of what I see and when the world doesn’t exactly fit those models, it is a question of an irrational world, really. Nothing to see or change with my rather scientific and close to artistic models or valuations. Unfortunately, someone failed to tell the markets that they should fit my idealised versions of rationality. The continued volatility and prices that trade away from what I deem to be intrinsic value is beyond my comprehension. Sarcasm aside, this is probably the greatest learning curve that investors have to go through. I still remember my early days in the market and the bad taste in the mouth that comes with seeing red. The saying I should have put up on my wall is a Benjamin Graham/Warren Buffett one: In the short-run, the stock market is a voting machine. Yet, in the long-run, it is a weighing machine. Also, someone should have told me that volatility is a part of a healthy market even if us homo-sapiens are not naturally wired to handle a world in constant flux. Markets do not go up or down in a straight line (though our first sell-offs often feel like it). Sitting on the sidelines because you’re bearish is also not usually the best of options. A younger me would’ve perhaps better understood the following logic. Between May 2008 and February 2009, in the depths of the GFC, the MSCI World lost -30.4%, but by the end of 2009 it had bounced back +40.8%. By all means, if you have a crystal ball and can time your entries and exits perfectly then do so but that might be a touch time consuming with today’s volatility. At the end of the day time IN the market is key. Which brings us to our next point... 2) Believe in the 8th wonder It baffles me constantly that the young are the most impatient, whereas one would expect from a pure numbers perspective it should be the other way around. Always in a hurry to put our fairly gotten-gains to work and turn them into ill-begotten ones. Sometimes I wish my 18-year old self truly understood the adage that it’s not timing the market, young chap, but time in the market that makes all the difference. Don’t work so hard that you cannot actually let your capital do some of the heavy lifting for you. The below chart is just one that illustrates this point. It shows the best and worst returning stretches over different time periods since the year 1970 (MSCI World). The hardest thing (which, by the way, shouldn’t be so hard if you have youth on your side) is to sit through the negative years, which do happen from time to time, and remember that over any given 10-year period since 1970 they still delivered at least a *cough* +0.21% return *cough*. In the approximate words of my forbearing forebear who is a rather big fan of George Bernard Shaw or Oscar Wilde (depending on who you believe said it), youth is wasted on the young. Annualised returns for MSCI World index since 1970  Source: tilney.co.uk I really do wish that I had started reading the Berkshire Hathaway Annual Letter earlier in my life. In one of the more recent ones that I recollect, the man showed that a 20.3% p.a. compound return since 1965 has today resulted in a cumulative return of 2,744,062%. Not too bad for buying mostly (no investor is perfect) quality companies and having a little patience. Granted, one cannot hope to consistently beat the S&P500 by double over that long a period. But! Even for us mere mortals, a 10% return over the same time frame should yield 5,700% (this, by the way, is the annualised return of the S&P500 up until 2019). The key here is to 1) find companies and investments that you can substantiate; and 2) to avoid the pitfalls of short-termism and loss of conviction. Markets by the way are great at pushing the weary away, whether it is head faking on the way up or misleading you through short-term price moves. Always buy good businesses at a fair price and let them do the work. 3) Every crisis is an opportunity One of the key thematics that I’ve seen through every crisis is that disruption is accelerated. Innovation flourishes. Think about technology post-dotcom bubble or the catalysation for the Zooms and biotech stocks of the world post-covid (granted we’re not there yet). If you want to go even further in history, and forgive us for being callous, think about how many of our technologies, including the jet engine (hello, recently reinvigorated space race!), came out of World War II. The development of the internet’s ancestor (ARPANET) was funded by US Department on Defense contracts in the late 60s (right in the middle of a rather frosty “war” that spilled over to Vietnam). Israeli’s happily point to their hazardous geopolitical situation as one of the main reasons that they are such an innovative and productive economy. Crisis breeds disruption and innovation. For the present here are some trends one can reasonably assume have been given a boost (the reality won’t be evident for a little while):

From an investment perspective, this downside has the benefit of creating some great winning thematics and strategies for the discerning long-term investor.  4) Be wary of your cognitive biases

(Related bonus: there’s always someone smarter or with better information) I don’t know how many of our readers actually remember their first investment, but this is always crucial. I personally wish that it had been a bad one and I was taught a lesson. But unfortunately, it was a fabulous one that made me blur the lines between luck and skill and then subsequently spend over a decade trying to replicate that exact scenario. By the way, and I am quite sure my colleagues are rather sick of hearing it, it was a little company I bought in the 5-10c range and took profits at $2.20 (that were subsequently mostly lost via hubris masquerading as investing as I chased the same kind of returns). I let greed overrule my more rational thought processes. In hindsight, I should actually have let the investment play out further. There was no reason grounded in logic to take those profits, the thesis was still intact. The stock now trades at over $13. I carry those lessons with me at all times, just ask some of my colleagues. The key here is to know that you will make mistakes, be aware of them and learn from them. One other bias we constantly see is confirmation bias, having a view and then essentially seeking evidence to back up said view. This is often seen when investors try to make predictions on the broader economy or when trying to time the market. Understand that the beginning has to be evidence-based and one has to constantly question their own assumptions every step of the way. In my own case above, it was to confirm my own supposed genius after the initial investment. The hubris and cumulative losses were in direct proportion to the ability to go out and find evidence to confirm my own views. There are many cognitive biases one needs to be aware of, here are a few you should look up and consider how they apply to you and the decisions you make when investing:

These are just a few examples (with limited explanations), just don’t forget to consider how biases are affecting your decisions.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim