|

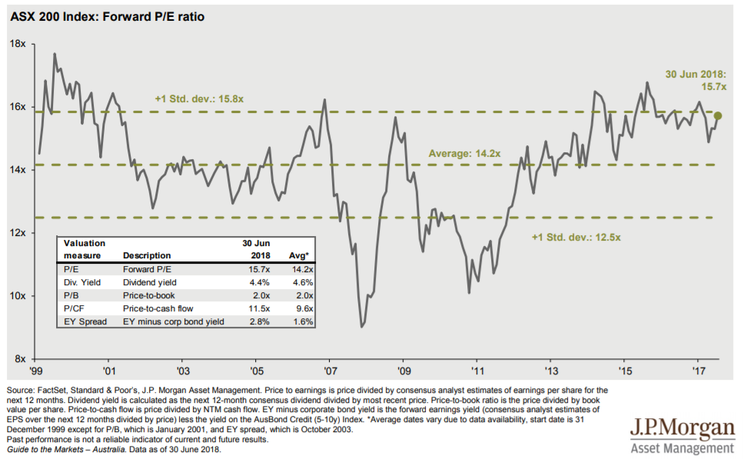

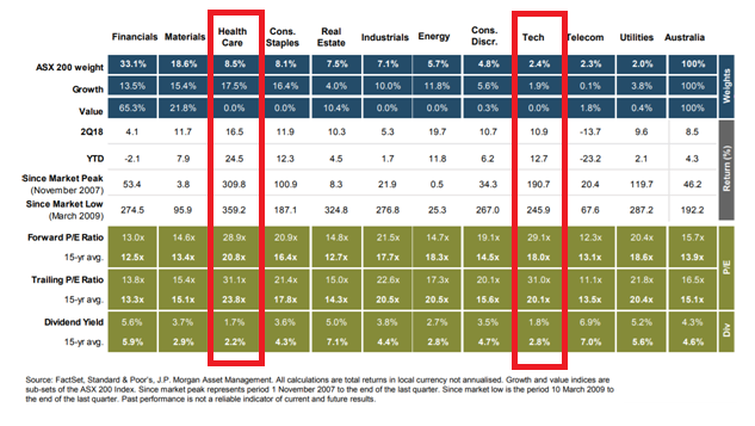

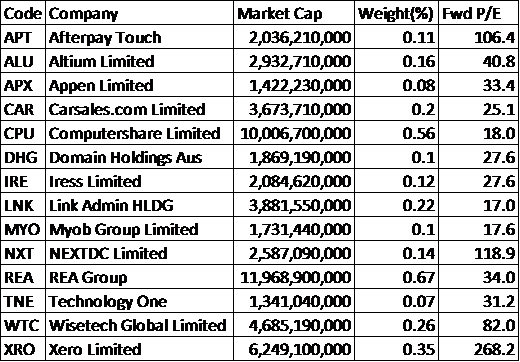

Guy Carson examines the current state of valuations in the Australian market. Some might argue that more than just a couple of stocks are looking a bit pricey. There is an old saying in financial markets – “Don’t stand in the way of a Bull Market”. This phrase essentially highlights the importance of momentum in the share market. Markets and stocks can run harder and further than anyone expects. Likewise on the downside they can fall more quickly and further than people realise. Whilst share price momentum is important and some investors choose to chase it, ultimately earnings will dictate where share prices go. The question then becomes have earnings gone up enough to justify some of the returns we have recently seen? When one looks at the forward P/E ratio for the Australian equity market over the last 20 years, one would conclude we are at the top end of the historical trading range. Given official interest rates sit at 1.5%, it is probably not suprising that equity valuations have risen. Investors have been forced into riskier asset classes such as Shares and Property in order to achieve some return on their capital. Currently at 15.7x, we are well ahead of the average of 14.2x but it doesn’t appear alarmingly so.  Source: JP Morgan Interestingly, the above chart shows the difference between the two major share market declines over this period. The “Tech wreck” which started its decline in 2000 was precedent by record multiples. The problems back then were primarily valuation driven and the following declines were purely a rerating. The 2007-2008 period was different, there was little “irrational exuberance” but there was significant financial engineering used to create earnings. The re-rating of shares leading into this period was significantly less than the previous market rally however the earnings ended up being of lower quality. With all of this history in mind the current valuations, when placed in the context of low interest rates, may appear slightly overvalued but not excessively so. However, when we delve below the surface of the index we do find some pockets of what we would consider extreme valuations. These are most notably in the Healthcare and Technology sectors.  Source: JP Morgan In recent years, earnings growth in Australia (and also globally) has been difficult to find. As a result investors have increasingly crowded into those sectors that do offer global tailwinds and earnings growth for the foreseeable future. In the US we have seen the rise of the FANGs and in Australia a small number of Technology companies have been chased by investors for access to that theme. The technology sector has seen a significant rerating and now the forward P/E stands at 29.1x well above the 18.0x average for the last 15 years. On an individual basis, the story gets even worse with the only stocks trading below 20x are the financial based companies (Computershare, Link Admin) and MYOB which continues to lose market share to Xero. Three companies have P/Es of over 100x and a further five have P/Es of over 30x.  Source: Thomson Reuters The healthcare sector has also seen a rerating as investors have sought out the high quality names in that space. The P/E of that sector is currently standing at 28.9x ahead of the 15 year average of 20.8x. Australian investors have been attracted to the quality in the space. In fact, we would say the healthcare space is the one area in Australia where we do have globally dominant names listed here. The likes of CSL, Cochlear and Resmed are unparalleled amongst listed Australia companies but at current multiples (34x, 30x and 38x respectively) we are not convinced they are sensible investments at this point.

We understand why investors have chosen these sectors. Healthcare and Technology both have global tailwinds set to drive the sectors forward in coming years. At the start of last year we highlighted that the Technology sector was our biggest exposure (see here). We also highlighted last year both the Healthcare and Technology as potentially attractive investments with a struggling Australian economy (see here). We fundamentally like these sectors but the valuations in our opinion have gotten ahead of themselves. As the valuations in these sectors have risen, investors have started to switch elsewhere. Sectors such as Consumer Staples have had strong runs and now trade on significant premiums to their historical averages. This has been driven by reratings in Wesfarmers and Woolworths despite increased competition. Only two sectors in the ASX200 currently trade below their 15 year average - Telcos and Energy. Telcos have suffered on the back of the transition to the NBN as well as increased competition in the mobile space. The sector still faces years of declining earnings ahead of it. Energy is a different story. A number of the leading companies in Australia (Woodside, Origin, Santos, Oil Search) have undertaken large LNG projects in recent times. In the lead up to the completion of these projects, the share price of each company starts to reflect the future earnings. The result is near term earnings multiples are high and hence the 15 year average is potentially overstated. With a lack of projects currently under consideration, the earnings multiple is less buoyant. We would look at the energy sector as fairly valued currently and would expect short term moves to come from fluctuations in the oil price. The sector that is trading on the lowest absolute multiple is the financials at 13.0x. This is still above its historical average and is obviously weighed down by the heavy weight to the banks. Our banks, whilst more or less in line with their historical valuations, are amongst the most expensive in the world (see here). We don’t see huge valuation risk within the banks but we do see earnings risk as a long super cycle comes to an end (see here). It is becoming increasingly difficult to find value in the Australian market. Low interest rates have forced investors into risky assets and prices have been bid up. Whilst the overall market ratios don’t appear to be overly stretched, high quality companies in the Technology and Healthcare sectors have created pockets of significant overvaluation. The reality is that the level of overvaluation is one we haven’t seen in around 18 years. Technology and Healthcare are sectors that we like on a fundamental basis and had a significant exposure to 18 months ago. We have reduced that exposure over the last six months and have rotated into more defensive sectors such as Utilities as well some smaller Technology stocks that have not participated in the recent rally. Whilst we potentially started rotating the portfolio a little early, we believe that is preferable to being late. This is due to another old saying in financial markets, “Up the stairs and down the escalator.” At some point valuations will matter and when that time comes, we’d rather not have exposure to expensive stocks.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim