|

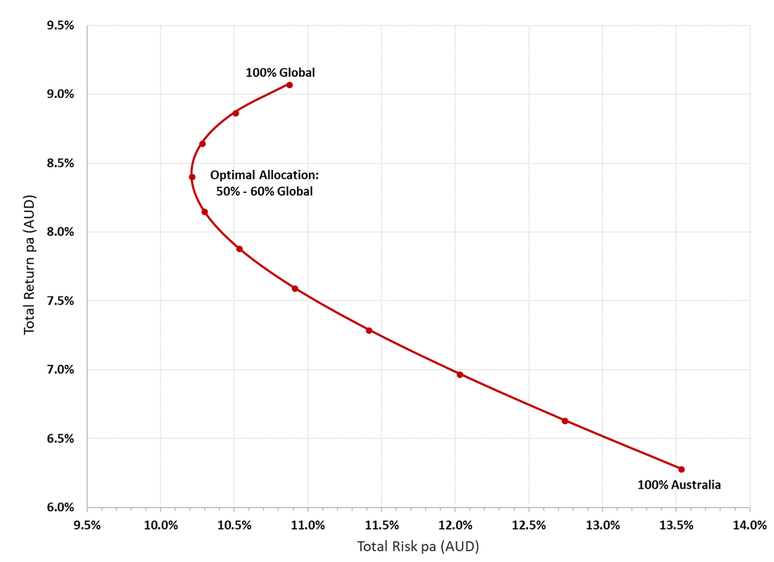

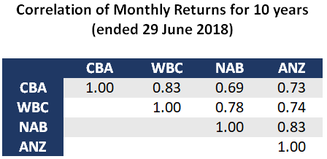

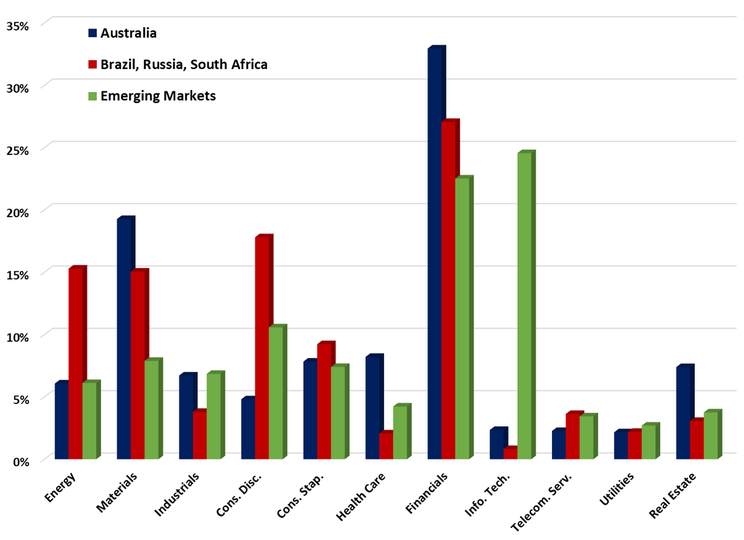

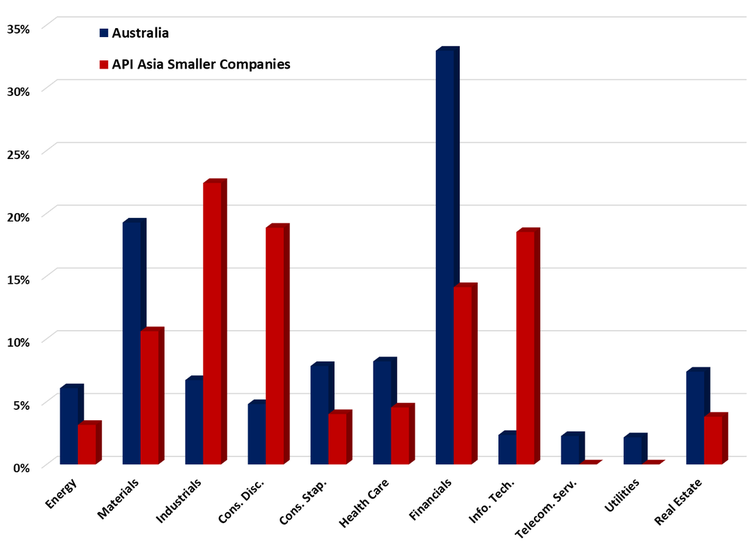

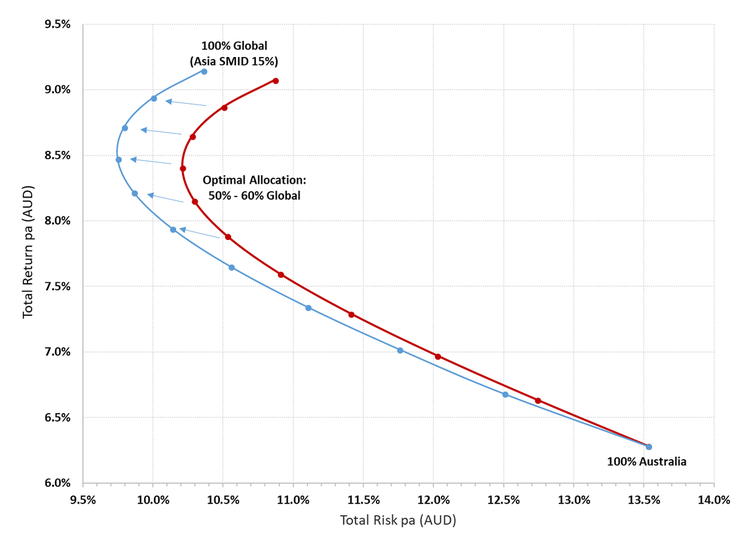

Robert Swift looks at the lack of diversification in not only the Australian market but also emerging markets. He presents an often misunderstood and underutilised alternative. We are going to briefly examine why diversifying into Emerging Markets is tempting, but potentially a mistake for Australian based investors. First let’s recap on some basics of portfolio construction. You should want to make as much money as possible but be aware that the volatility of your return matters. It’s return on volatility (risk) that counts most. For professional money managers a portfolio is not just a collection of ‘good ideas’ but a combination of stocks whose attributes in combination provide the best prospects for a high return on risk taken. Consequently adding global equities to an Australian portfolio is a good idea. Even if their future returns are lower than their past returns and now ‘only’ equal to future returns on Australian equities, this is still sound practice. Check out the range of returns and risks in the chart below which combines Australian with global developed market equities (represented by the ASX300 and MSCI World total returns in AUD terms) in varying proportions for the 10 year period ending 29 June 2018. Although this is based on actual returns there is no reason to doubt that the future will not show similar diversification benefits from adding international shares to an Australian portfolio. Getting your portfolio ‘up and to the left’ should be everyone’s goal.  Source: Thomson Reuters We think it is pretty well understood that the Australian equity market is dominated by banks and resource companies. It also used to have a large telco exposure too however the shrinkage in market capitalisation of Telstra has made it much lower in terms of its index weight. The demise of Telstra is testimony to the dangers of under-investment and over distribution of dividends; and we may revisit that as a general issue for all companies in a future article. Australia isn’t the only place where companies have been over distributing and underinvesting; the UK is another. Some countries such as Japan have had the opposite problem. For most investors owning the Australian banks is effectively a way to get exposure to dividends which increasingly depend on profits made from, less bad debts provided for, Australian housing loans. Given that most people’s major store of wealth is in their own home, owning lots of Australian banks in addition, represents a bad idea. You own your own home and then get exposure to the house price trends of other people’s homes. It is a duplication of risk. Some investors argue that they are diversified by owning all four major banks but from the table below you can see that they tend to behave in a very similar fashion to each other.  Source: Thomson Reuters Even owning all four banks represents the same ‘bet’ and doesn’t help your overall portfolio of wealth especially if you include property assets in the mix, as you should. So why are Emerging Markets a bad diversification decision for Australians? They are international and represent and operate in faster growing countries so why not have a dedicated allocation to them? It is a sub optimal decision because the composition of many of these equity markets is very similar to the Australian market; especially some of the major ones such as Brazil, South Africa and India which, like Australia, are financial resource and utility heavy while also being net debtor countries, like Australia. See the table below which shows the sector weights for Australia compared to Brazil, South Africa and Russia. We also compare this to the broader group of Emerging Market countries.  Source: Thomson Reuters If something happens to iron ore prices it is likely to affect CVRD in Brazil and Rio in Australia in the same way. If global liquidity tightens (it will) and banks in net debtor nations (such as India, Brazil, Turkey, Australia) find it harder to secure deposits, then this too will cause similar effects in financials operating in all these countries. Net foreign assets (NFA) is a simple but underutilised way to assess the likelihood of capital flight or vulnerability to rising interest rates. It is simply a country’s asset stock less its liabilities to foreigners. Running persistent current account deficits will add to liabilities; surpluses will add to assets. At some point, seriously negative NFA countries will most probably see downward currency pressure to realign the assets and liabilities. Reducing the currency will increase the value of the assets and reduce the value of the assets held by foreigners. Australia’s net liabilities are almost a trillion A$. The size of the economy is about A$ 1.6 trillion. As a % of GDP it is about 60%. Brazil is about – 35%; Turkey (which has suffered tremendous currency depreciation already ) is at – 55%, similar to Australia. By comparison, Japan is a net creditor nation with net foreign assets of over US$3 trillion, approximately 65% of its GDP. There is a lot of Japanese debt BUT they own a lot of foreign assets too. Therefore think of investing in Brazil, Mexico, Turkey etc as owning a set of stocks which are likely to move up and down in similar fashion to those in your Australian equity portfolio. Some people argue that higher economic growth will compensate for this correlation risk but this is not necessarily true. Good long-term returns are derived from investing at low valuations with a lack of asset confiscation through debt default, inflation and currency depreciation; or forced seizure of assets. These last three tend to occur when the macro picture is very stressed. If you care to read about Turkey and the Turkish Lira, this is a classic example of an emerging market with decent demography; reasonable GDP growth, but a seriously indebted country which is very vulnerable to capital flight; happening now on a grand scale and causing well founded fears of asset seizure. We are NOT claiming what is happening in Turkey is about to happen in all emerging markets, but adding all emerging markets to Australian equities exposes your portfolio to many of the same risks in countries with similar indebtedness and risk of downward currency pressure. As an asset allocation it is not a good idea. What is a good idea is to gain better diversification while investing at relatively cheap prices. You can achieve this by investing some of your portfolio into small caps in Asia including Japan. As smaller companies they tend to be less exposed to global factors; less vulnerable to government interference; more dynamic and faster growing; and most importantly for an active manager, inefficiently and incorrectly priced. This is true of Asian smaller companies which we believe should be considered as a place for Australian investors to allocating some of their hard-earned savings. Check out the sector weights of Asian smaller companies and see how they are different from Australia – thus providing genuine diversification.  Source: Thomson Reuters We also generated an efficient frontier over the same timeframe as the earlier chart with combinations of Australian and Global equities where the non-Australian allocation is a combination Global large caps and Asian small/mid over the same 10 year time frame to 29 June 2018.  This chart demonstrates how Australian investors with BOTH Global and Asian small caps can improve portfolio risk-return characteristics. Asian smaller companies tend to behave differently from Australian companies AND differently from global large companies. This is a good thing.

Finally we point out both the cheap valuations of Asian smaller companies and our Asian Small Cap strategy with PE ratios of approximately 10.2x and dividend yields of 3.2%, and the fact that they are very innovative with the majority of patent applications coming from this sector. So as you increase your international allocations, and undoubtedly receive advice to add emerging markets, think again. Much better to achieve decent returns from quality Asian small companies which are operating in economies with sound fiscal positions; economies with less risk of capital flight and currency depreciation; and more innovation. As we say, by choosing Asian smaller companies, you ‘invest today in the companies of tomorrow’.

3 Comments

Jim winten

19/7/2018 05:43:37 pm

Good stuff as more portfolio education is needed - would you be interested in speaking to 60 investors in Toowoomba as we meet each Wednesday?

John Palmer

20/7/2018 09:16:14 am

Great to see you enjoyed the read Jim, I will be in touch later today to tee up some presentations

Ian Newbery

24/7/2018 04:02:28 pm

More knowledge like this is what we all need. Your comment will be posted after it is approved.

Leave a Reply. |

Markets & CommentaryAt TAMIM we are committed to educating investors on how best to manage their retirement futures. Sign up to receive our weekly newsletter:

TAMIM Asset Management provides general information to help you understand our investment approach. Any financial information we provide is not advice, has not considered your personal circumstances and may not be suitable for you.

Archives

April 2024

Categories

All

|

RSS Feed

RSS Feed

TAMIM | Equities | Property | Credit

DISCLAIMER

The information provided on this website should not be considered financial or investment advice and is general information intended only for wholesale clients ( as defined in the Corporations Act). If you are not a wholesale client, you should exit the website. The content has been prepared without taking into account your personal objectives, financial situations or needs. You should seek personal financial advice before making any financial or investment decisions. Where the website refers to a particular financial product, you should obtain a copy of the relevant product services guide or offer document for wholesale investors before making any decision in relation to the product. Investment returns are not guaranteed as all investments carry some risk. The value of an investment may rise or fall with the changes in the market. Past performance is no guarantee of future performance. This statement relates to any claims made regarding past performance of any Tamim (or associated companies) products. Tamim does not guarantee the accuracy of any information in this website, including information provided by third parties. Information can change without notice and Tamim will endeavour to update this website as soon as practicable after changes. Tamim Funds Management Pty Limited and CTSP Funds Management Pty Ltd trading as Tamim Asset Management and its related entities do not accept responsibility for any inaccuracy or any actions taken in reliance upon this advice. All information provided on this website is correct at the time of writing and is subject to change due to changes in legislation. Please contact Tamim if you wish to confirm the currency of any information on the website.

magellen, kosec, clime, wilson, wam, montgomery, platinum, commsec, caledonia, pengana, tamim